If you do your taxes online or through a registered tax agent, you no longer need a Latrobe Health Services tax statement.

For this reason, we don’t automatically send you a tax statement, however you can still download or request one.

Please note that from 1 July 2024, the Medicare Levy Surcharge (MLS) income thresholds have changed. To know more about these 2024-25 financial year MLS income thresholds visit the Australian Taxation Office’s website.

Why don’t I need a tax statement?

We send your tax statement information directly to the Australian Tax Office. This is because the Australian Government made changes in 2019 to make health insurance simpler (yay!). This means that if you’re doing your taxes online or with a registered tax agent, your private health insurance details will automatically prefill.

When will you send my tax statement details to the ATO?

We’ll send all the tax statements by 7 July. Your tax statement won’t be available until this date.

I still want a copy of my tax statement. How do I get it?

You can get a copy of your tax statement a number of ways. Remember it will not be available until 7 July.

Get a copy of your tax statement by logging into your online account

- Log into your online account

- Navigate to "Documents"

- Select Tax Statement 2025

- Click on the view next to the name of the member you wish to access the tax statement for

- The statement will load.

There is only a tax statement for me and my partner but not my adult child – where do I get this?

Only members and spouses are eligible for tax purposes. Any dependants on the policy will not be able to claim this for tax purposes.

Get a copy of your tax statement by sending us a contact enquiry.

If you haven’t set up your online account, we can help you do that. If you’re having trouble getting a copy of the tax statement, send us a request using this contact form and we will email a copy to you.

Alternatively, you can log in to your account and access your tax statement.

I want to update my Australian Government Rebate Tier

Sure thing. Send us a request using this contact form and one of our team will be in touch.

I need help doing my tax return

The best place to go for help for your tax return is the ATO or your registered tax agent. You can contact the ATO on 13 28 61 or visit the myTax website.

Understanding your statement

How to read your tax statement

Here’s what you need to know about your tax statement and use this information to fill in your tax return. If you do your tax online or see a registered tax agent, this information is automatically pre-filled and you do not need a copy of the tax statements

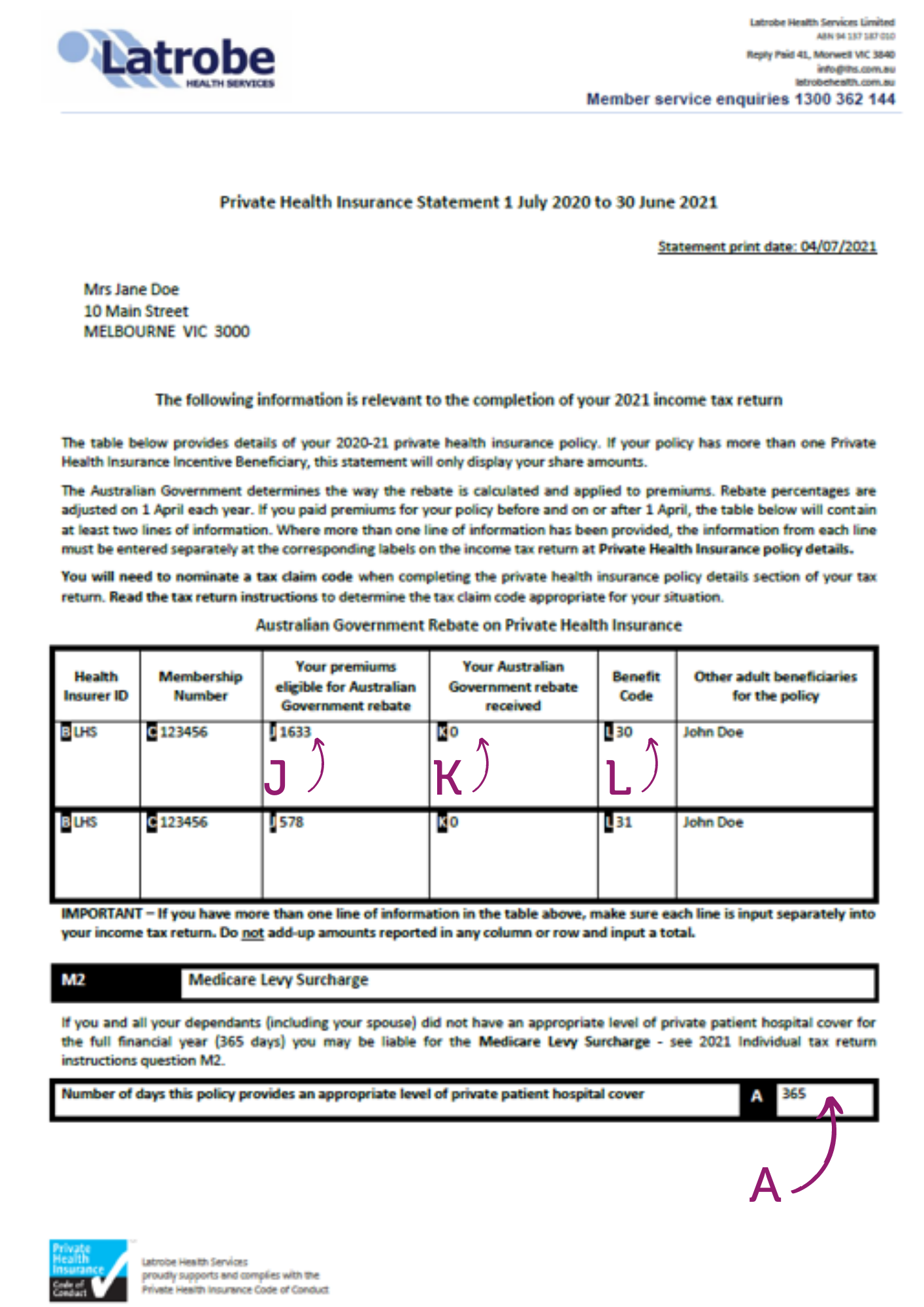

What does J mean?

J only shows premiums paid in this financial year and does not reflect the premiums on the membership for that financial year. For example, if you paid in June 2023 for 12 months, then not pay again until July 2024 – your statement will show 0 as you have not paid any premiums in the financial year.

What does K mean?

K represents the amount the Government has paid towards your share of the policy. If you're not registered for the Australian Government Rebate on private health insurance as a premium or are on Tier 3 of the income bracket, this amount will be $0.

What does L mean?

L represents the rebate you are entitled to, based on your age.

What does A mean?

The figure at A is the number of days you had private hospital cover in the last financial year. If this amount is less than 365 days (or 366 days in a leap year), and you earn above the income threshold, you may have to pay the Medicare Levy Surcharge.